Calculating your company’s days sales outstanding (DSO) can create meaningful insights to support your business strategy. Your DSO tells you the average time it takes to collect payment after a sale. With a simple number, you can learn more about your sales team and the sales cycle, your customers and their buying abilities, and your industry and the effect of seasonality.

Most critically, better understanding your DSO helps finance leaders determine cash flow health, navigate the trade-offs between customer flexibility and fast collection, and discover solutions that eliminate those trade-offs entirely.

What is Days Sales Outstanding (DSO)?

Days Sales Outstanding (DSO) is a critical financial metric that measures the average number of days it takes your company to collect payment on accounts receivable (or after making a credit sale). Simply put, it tells you how long your money stays tied up in unpaid invoices before converting to cash.

DSO serves as both a performance indicator for your accounts receivable management and an early warning system for your business. It’s also a key metric in financial reporting, as accounts receivable represents a significant balance sheet asset that investors and lenders closely monitor for liquidity assessment.

A low DSO signals high collection efficiency and strong customer relationships. A rising DSO can indicate potential problems with customer creditworthiness, internal collection procedures, or market conditions before they impact cash flow.

For growing businesses, DSO directly impacts your ability to reinvest in operations, pay suppliers, and fund expansion. Companies that consistently convert sales to cash quickly maintain better liquidity, reduce borrowing needs, and create more financial flexibility to capitalize on opportunities or weather unexpected challenges.

DSO Calculation Methods & Examples

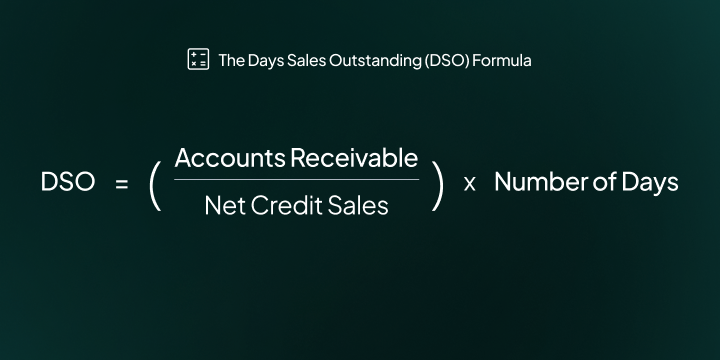

The Days Sales Outstanding Formula

Days Sales Outstanding (DSO) = (Accounts Receivable/Net Credit Sales) x Number of days

An example:

During the last three months of the year, your company made a total of $2,000,000 in credit sales and had $1,000,000 in accounts receivable. The time period covers 90 days. Your company’s DSO for that period is calculated as follows:

- 1,000,000 divided by 2,000,000 equals 0.5.

- 0.5 multiplied by 90 equals 45.

- The DSO for this business in this period is 45.

- DSO = (1,000,000/2,000,000) x 90 = 45 days

This means that it takes approximately 45 days to receive payment on your credit sales.

How to calculate your days sales outstanding ratio (DSO)?

Steps to calculating DSO:

- Gather Your Financial Data Collect your accounts receivable balance and total credit sales for the same time period from your financial statements. Ensure you're using net credit sales (excluding cash sales) for accuracy.

- Determine Your Time Period Choose your measurement period - typically 30 days (monthly), 90 days (quarterly), or 365 days (annually). Most businesses calculate DSO monthly for regular monitoring.

- Apply the Formula DSO = (Accounts Receivable ÷ Net Credit Sales) × Number of Days in Period

- Calculate and Interpret Divide your accounts receivable by net credit sales, then multiply by your chosen time period. The result tells you the average number of days it takes to collect payment after a sale.

Another example, this time of the monthly DSO ratio for a SaaS company:

- Accounts Receivable: $2.4 million

- Net Credit Sales (last 30 days): $2.4 million

- Time Period: 30 days

- DSO = ($2.4 million ÷ $2.4 million) × 30 = 30 days

This SaaS company collects payment in an average of 30 days after signing new contracts, which is well within the typical 30-45 day range for software businesses. This suggests efficient invoicing and collection processes for their subscription and enterprise licensing revenue.

Advanced DSO Calculation Methods

While the standard DSO formula works for most businesses, two alternative approaches can provide more nuanced insights:

Count-back Method: Instead of using average sales, this method works backward from your current accounts receivable to determine exactly which invoices are outstanding. This provides more accurate results for businesses with fluctuating monthly sales.

Best Possible DSO: Calculate your DSO using only current receivables (excluding past-due amounts) to understand your baseline collection efficiency without the impact of problem accounts.

Period-Specific Considerations

- Monthly DSO: Best for ongoing monitoring and quick course corrections

- Quarterly DSO: Smooths out monthly fluctuations and seasonal variations

- Annual DSO: Provides the most stable benchmark for year-over-year comparisons

Choose your calculation period based on your business needs - monthly for active management, quarterly for trend analysis, and annually for strategic planning.

What's considered a low DSO and a high DSO?

When evaluating your DSO performance, it helps to have a baseline for comparison.

The industry average days sales outstanding ratio is considered to be 36.6. Taking this into consideration, anything below 36.6 is considered a low DSO, and anything above 36.6 is considered a higher DSO. This number varies by industry and by company size, so it’s important to determine a DSO ratio that is reflective of your own business.

Elements like industry specific targets, company size, or seasonality impact what determines a healthy DSO for your business. Since an ideal DSO isn’t one-size-fits-all, the next section dives into detailed insights for building the most informed DSO strategy.

Determining a Healthy DSO Ratio for Your Business

Although the industry average for a days sales outstanding ratio is 36.6, this doesn't always meet expectations if you have longer repayment terms with your customers. If you expect your customers to fully repay within 90 days and you have a DSO ratio of 62 then you're well within the repayment time period and are probably maintaining a healthy cash flow.

DSO Ratio Benchmarks by Industry

Payment cycles vary significantly across different sectors due to unique business models, customer types, and standard payment terms. Some industries like retail have faster consumer payment patterns while professional services payments are often connected to project-based billing cycles. Below you can see how benchmarks vary greatly by the nature of the business.

Technology/Software: 35-50 days

Professional Services: 40-60 days

Retail/E-commerce: 15-25 days

Manufacturing: 45-65 days

Source: Hackett Group

Understanding where your business falls within these industry ranges helps determine realistic DSO targets. It also helps in identifying whether your current performance signals potential cash flow concerns or operational efficiency opportunities.

An analysis of the top 1,000 U.S. public companies shows that top-performing companies collect payments 41% faster than typical companies (29.0 days versus 48.8 days), showing the opportunity for improvement no matter your industry.

Company Size Considerations Related to DSO

Your company's size directly influences a realistic DSO target. Smaller businesses typically need faster collection cycles to maintain healthy cash flow, while larger enterprises may accept longer payment terms as part of strategic customer relationships.

- Enterprise companies often have the leverage to implement robust collection systems and dedicated accounts receivable teams. They may also extend 60-90 day payment terms to secure major contracts.

- Mid-sized businesses usually operate within standard 30-45 day terms, balancing customer satisfaction with cash flow needs.

- Small companies frequently require payment within 15-30 days simply to survive, making focused collection processes a requirement.

The critical factor isn't achieving the lowest possible DSO, but instead optimizing collection strategies connected to your company's size, resources, and customer relationships.

A 45-day DSO might represent excellent performance for a growing mid-market company, while the same number could signal collection problems for a small business with limited cash reserves.

Seasonal Variations Influence DSO

Many businesses experience expected DSO fluctuations throughout the year that don't necessarily signal collection problems. End-of-quarter payment rushes, holiday shopping cycles, and industry-specific patterns can temporarily affect collection timing.

The key is establishing your business's normal seasonal range across multiple quarters. If your DSO typically rises from 35 days in Q2 to 42 days in Q1 due to customer payment timing, factor this into cash flow planning rather than treating it as a collection crisis. When seasonal increases exceed historical patterns by more than 10-15%, that's when investigation becomes necessary.

A DSO Ratio of Zero

There are circumstances where a DSO number can be zero. This occurs when sales aren't classified as credit sales. Cash sales have a DSO of zero because they don’t affect account receivables and the time it takes to recover payment. This is common in retail where you purchase an item instantaneously or if you sell a solution that is only accessible after full payment is received.

What does a low DSO mean?

A low DSO value can be interpreted as a successful collections process where a company is efficient at collecting outstanding payments. A company with a low DSO might have techniques to encourage timely repayments of customer credit, like early payment discounts, annual contract discounting, or leverage embedded financing solutions like Gynger.

What does a high DSO mean?

Ultimately a higher DSO number reflects that a company is waiting a long period of time to receive funds for its credit sales. When a DSO number is higher a company needs to be mindful of its cash flow and ensure that it has enough runway in the bank to mitigate costs until payment is received for its services or products. For technology companies, a high DSO is particularly problematic since you often need cash for product development, talent acquisition, and rapid scaling.

How DSO Connects to Other Key Financial Metrics

DSO doesn't operate in isolation. It's a crucial component of your broader financial ecosystem that directly impacts cash flow, working capital, and overall business health.

Cash Conversion Cycle (CCC)

The cash conversion cycle which measures how long it takes to convert investments into cash returns. Your DSO is one of three key elements in the cash conversion cycle.

The CCC formula:

CCC = DSO + Days Inventory Outstanding (DIO) - Days Payable Outstanding (DPO).

For software companies, your cash conversion cycle is streamlined when you don't carry physical inventory.

Your CCC becomes: DSO - Days Payable Outstanding (DPO), where DPO reflects payments to vendors like cloud providers, contractors, and service suppliers.

Many software companies have minimal DPO since most expenses are paid monthly, making DSO the primary driver of cash conversion. A SaaS company with a 30-day DSO and minimal supplier payment delays essentially has a 30-day cash conversion cycle - the time from sale to cash collection.

Accounts Receivable Turnover Ratio

This metric measures how efficiently you collect receivables throughout the year.

The AR turnover ratio formula:

AR turnover ratio = Annual Credit Sales ÷ Average Accounts Receivable

While DSO tells you the time element, AR turnover shows frequency. A DSO of 30 days typically corresponds to an AR turnover ratio of about 12 times per year. Improving one automatically improves the other.

Working Capital Impact

Every day you reduce DSO improves working capital efficiency by freeing up cash equal to your daily credit sales. If your business generates $100,000 in daily credit sales, reducing DSO by just 5 days releases $500,000 in working capital. That working capital can be reinvested in growth or debt reduction rather than sitting in unpaid invoices.

Understanding these relationships helps you see why DSO optimization isn't just about cash flow optimization. It's about maximizing your entire financial operation.

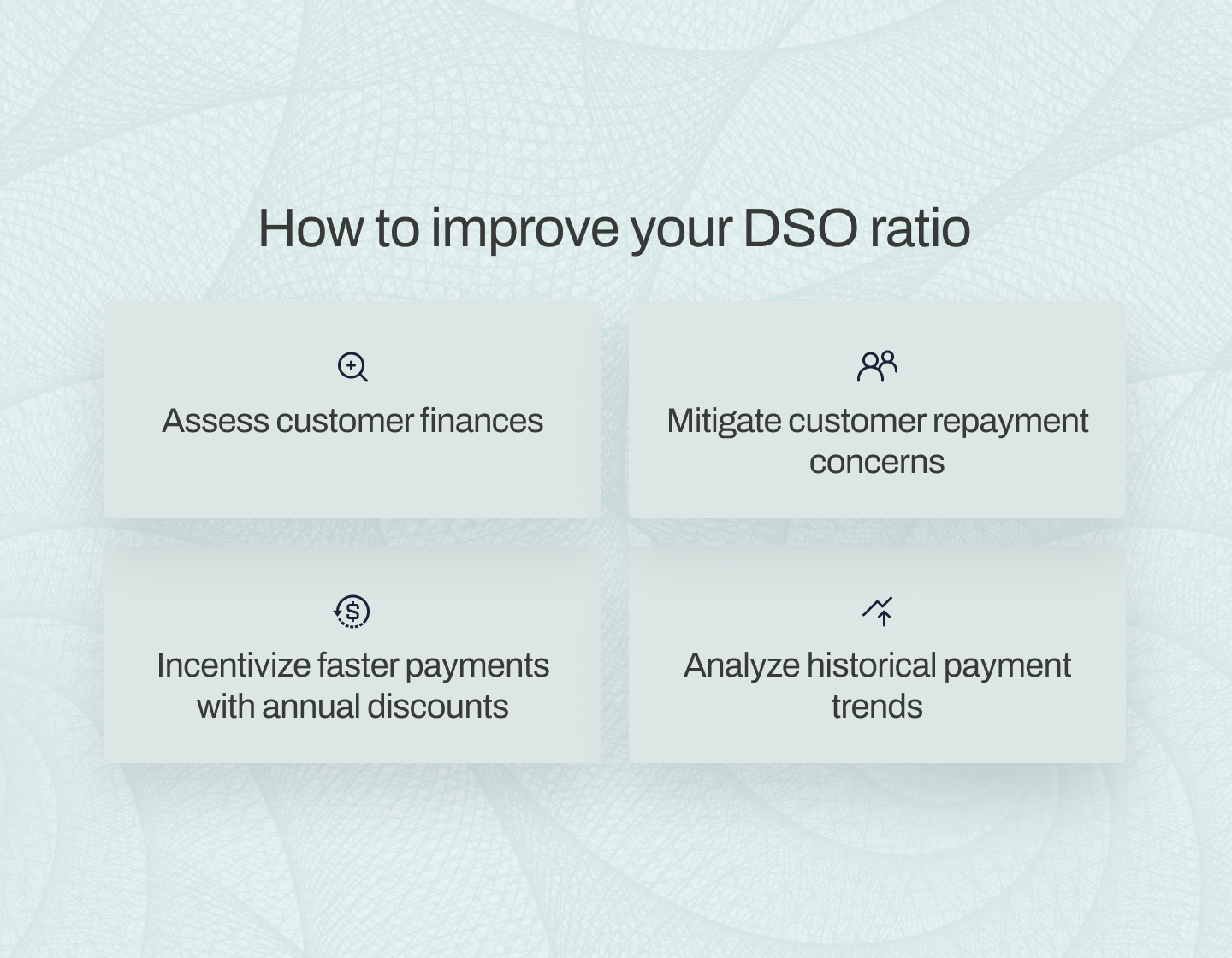

How to Improve Your DSO Ratio

If your company has a high DSO number and you are concerned about cash flow there are some techniques you can apply to streamline your collections process and improve your accounts receivables.

Assess customer finances

When conversations begin with a new prospect, one of the early steps should be learning more about their financial health. Especially if they need financing to support the purchase, you want to know more about them and the likelihood they’ll be approved for financing.

You can start by asking them further questions about how they are preparing to make repayments and what they’ve allocated from their budget for this investment. Once you have initial information from them, a soft credit check or financial research tool will help paint a fuller picture of their financial capabilities. Check with the tools you already have access to and see what they offer. For example, Gynger’s pre-approval process shows you up front what credit a prospect can access.

Mitigate customer repayment concerns

Once your customers have explored their financing options, you can help them feel more informed and at ease by sharing the specifics of what they’re purchasing along with a clear repayment summary. This reduces payment friction and makes the purchase process simpler.

If the customer has secured outside financing, you can help them with understanding how it relates to what they purchased. If you work with an accounts payable platform like Gynger, you’ll have direct insight into the different financing options available to them and go through the details with them step-by-step.

The aim is to make it an easy transaction for all parties. You can further mitigate concerns and create a smooth experience when you:

- Align on repayment terms that work for your company’s cash flow needs and your customer’s financial situation

- Provide multiple ways to pay invoices, whether through one-click payments or automated recurring setups

Gynger supports you in smoothing out the process with built-in customized re-payment options that tailor to the payback schedule and payment method that best works for your customer. It's a win-win solution that gives customers the flexibility they need while ensuring you get paid upfront.

Incentivize faster payments with annual discounts

Another angle to explore during payment term negotiations is structuring annual commitments that benefit both parties. While annual contracts can offer customers better value through improved packaging and product offerings, you can further accelerate your cash flow by adding early payment discounts to these deals. This creates a compelling reason for customers to pay upfront rather than spreading payments throughout the year.

This strategy works well if you don't have other payment tools at your disposal.

However, with a payments platform like Gynger, this trade-off becomes unnecessary. Your customers can enjoy the benefits of annual contracts while still paying over time, and your company receives the full payment upfront. This setup eliminates the need to sacrifice revenue through discounts to improve cash flow.

Analyze historical payment trends

When setting payment terms with customers, consider how seasonal patterns might affect both their payment behavior and your business cycles. Some customers may have tighter cash flow during certain quarters or delay payments around year-end due to budget cycles. Your own business may experience seasonal sales pushes or increased expenses around hiring, product development, or renewals that impact your cash flow requirements.

Use your historical payment data to identify these patterns and proactively address them during negotiations. If you know certain customer types typically pay slower during specific periods, and you anticipate your own seasonal cash flow needs, you can adjust your approach. Consider building in earlier due dates, offering seasonal payment schedules, or setting expectations upfront about timing.

Internally, make sure your finance and sales teams are aligned on how these seasonal fluctuations will impact your DSO reporting. Establish clear boundaries about acceptable payment terms during peak sales periods. This way, DSO changes can be properly explained to financial teams, investors, and leadership as expected business patterns rather than collection problems.

With Gynger, you can offer customers payment flexibility that works with their seasonal cycles while still getting paid immediately yourself. This eliminates both the customer relationship challenges and your own seasonal cash flow concerns.

How to Improve Your DSO Score with Embedded Financing Technology

The tactics necessary to lower your DSO ratio often involve creating new internal processes and building net new revenue capture and cash flow management strategies. They can also require different financing and payment tools all together.

Since developing financial products aren't the core competencies of your business, building them in house can take away valuable chunks of time and budget from your existing product roadmap. Instead, by leveraging embedded financing tools, you can offload the heavy lifting required to lower your DSO and focus on hitting your product milestones and growth targets.

Unlike traditional DSO improvement tactics that require process changes and customer cooperation, embedded financing offers a fundamentally different approach to DSO challenges. While conventional methods might reduce your DSO from 45 to 35 days, Gynger's embedded financing achieves instant cash conversion, effectively reducing your DSO to zero.

See how embedded financing helps improve DSO:

Simplify pre-qualification

With embedded financing technology, you can easily automate the buyer prequalification process. Pre-qualification involves assessing a customer's creditworthiness and determining their borrowing capacity before they commit to a purchase.

You won’t need to stress about gathering all of the right details up front, managing a credit check solution, or interpreting credit scores and financial data. Instead, your embedded financing platform should be able to handle this entire process automatically. This decreases your risk by ensuring customers can actually afford what they're purchasing and helps you properly prioritize deals based on their likelihood to close.

As you sync your CRM accounts or manually add them, technologies like Gynger pre-qualify your accounts in the background. This gives you better insights into your customers' financial capacity and creditworthiness before you even present pricing, allowing you to tailor your sales approach and payment options accordingly.

Diversify payment options and terms

In general, flexible payment terms allow your customers to choose payback periods that fit their business and financial needs. Embedded financing tools can support your business in offering these different deal terms. Gynger pays you your full contract amount instantly while still providing your customers with preferable payment terms to help close the deal faster. You can offer your customers net terms or monthly terms easily customizable within Gynger Pay.

Automate billing and collections

Some financing technologies only facilitate the payment and the collections remain the responsibility of the company. When you offer embedded financing to your customers using Gynger as soon as the customer is qualified for financing and accepts the terms your company is paid directly the full sum of your contract amount. The customer re-payments are then managed by Gynger removing any collections or repayment concerns.

Reach a Healthy DSO Ratio with Gynger

Traditional DSO improvement methods require ongoing effort, process changes, and constant monitoring to achieve modest results. Leveraging a payments and embedded financing platform like Gynger eliminates these challenges entirely by providing instant payment while maintaining customer flexibility.

Whether you're selling annual software licenses, multi-year enterprise contracts, or custom implementation services, Gynger seamlessly adapts to your technology sales cycles.

DSO = 0

Receiving payments instantly after your customer accepts your terms reduces your DSO value to zero.

Fast cash conversion cycle

Cash is instantly deposited within your bank accounts. This means your company has a higher level of financial health, supercharging your cash flow optimization.

Simplified accounts receivable management

Gynger handles the complete accounts receivable process on the customer side. No more leveling the balance sheet and chasing late payments.

Ready to eliminate collection delays and achieve zero-day DSO?

Gynger's embedded payments platform pays you the full contract amount upfront while giving your customers flexible payment terms they need, ultimately allowing you to close deals and secure renewals faster. No more chasing invoices, managing collections, or waiting 30-60 days for customer payments—you get immediate cash flow while customers pay over time.

See how you can accelerate accounts receivable and transform your cash flow with Gynger. Join growing companies who've already eliminated their DSO challenges. Explore Gynger Pay and start getting paid instantly.

Unlock the full article

This section is reserved for users. Sign in to continue reading or connect with our team to learn more.

Want to learn about how Gynger can help your business accelerate without compromise?

Get in touch