.png)

Clearly understanding the distinctions between receivable financing and factoring is essential to making informed decisions that optimize cash flow, preserve customer relationships, and maintain financial flexibility.

In this article, we will:

- Define receivable financing and factoring

- Compare them across multiple dimensions (structure, cost, control, risk, accounting)

- Explore when each is appropriate

- Highlight how Gynger’s model brings unique advantages, combining control, flexibility, and speed

What Is Receivable Financing?

Receivable financing (also called AR financing, invoice-backed lending, or accounts receivable financing) is a funding approach where a company uses its outstanding invoices as collateral to borrow money, while retaining ownership and control of those invoices.

How It Works

- Submit invoices or AR ledger to a lender.

- The lender provides a cash advance, often a percentage (e.g., 70–90%) of the invoice face value.

- The business continues to collect from customers as usual.

- When payments arrive, the company repays the advance plus interest, fees, or service charges to the lender.

Because receivables remain on the balance sheet and the company continues to manage collections, this model preserves internal oversight of financial operations and customer interactions.

Pros & Challenges of Receivable Financing

Pros:

- Maintains customer relationships and control over credit operations.

- Financing arrangements remain internal and confidential.

- Potentially lower costs than factoring due to retained control.

- Preserves working capital without immediate forfeiture of receivable value.

Challenges:

- Requires a robust internal credit/collections operation.

- Funding advance is contingent on the creditworthiness of customers.

- Default or delayed payments can affect repayment obligations.

- Receivables remain a liability on the balance sheet.

What Is Invoice Factoring?

Factoring involves the sale of receivables to a third-party factor. The factor purchases invoices, advances a portion of their value, and assumes responsibility for collections.

How It Works (Factoring Model)

- Sell unpaid invoices to the factor.

- Factor pays an upfront percentage (typically 80–95%).

- Factor manages collections and customer interactions.

- Once invoices are settled, the factor remits the remaining balance, less fees and reserves.

Pros & Challenges of Factoring

Pros:

- Immediate liquidity and certainty of cash inflow.

- Outsourced collections and credit management.

- Suitable for businesses lacking extensive internal credit capabilities.

- Scales efficiently with growing receivable volumes.

Challenges:

- Higher fees and discount rates compared to receivable financing.

- Customer relationships may be affected by third-party interactions.

- Disclosure to customers is often required.

- Loss of control over receivable management and potential exposure to restrictive covenants.

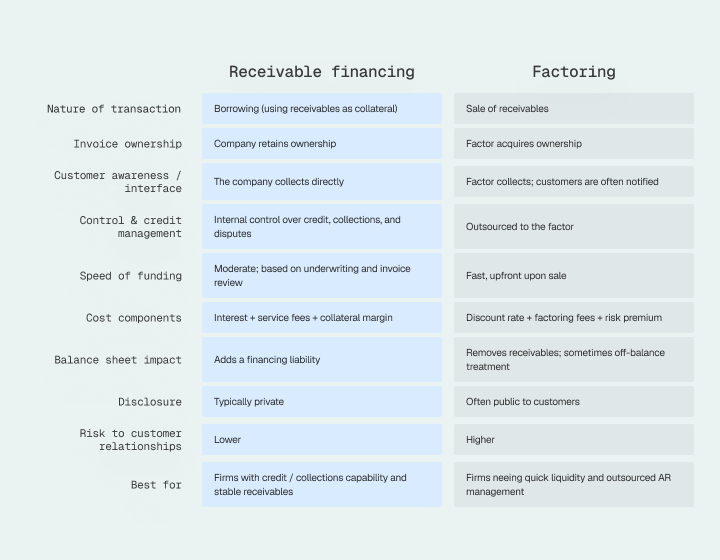

Receivable Financing vs Factoring: Side-by-Side Comparison

When Factoring vs Receivables Financing Makes Sense

Use Receivable Financing When:

- There is a mature credit function and a capable collections team.

- Receivables are predictable and backed by creditworthy customers.

- Maintaining customer relationships and internal process control is a priority.

- Minimizing customer disruption and preserving discretion are important.

- Cost efficiency is prioritized over speed of cash inflow.

Use Factoring When:

- Immediate liquidity is required.

- Internal credit management capacity is limited.

- Rapid scaling demands the outsourcing of AR operations.

- Trading margin or customer interface control for speed is acceptable.

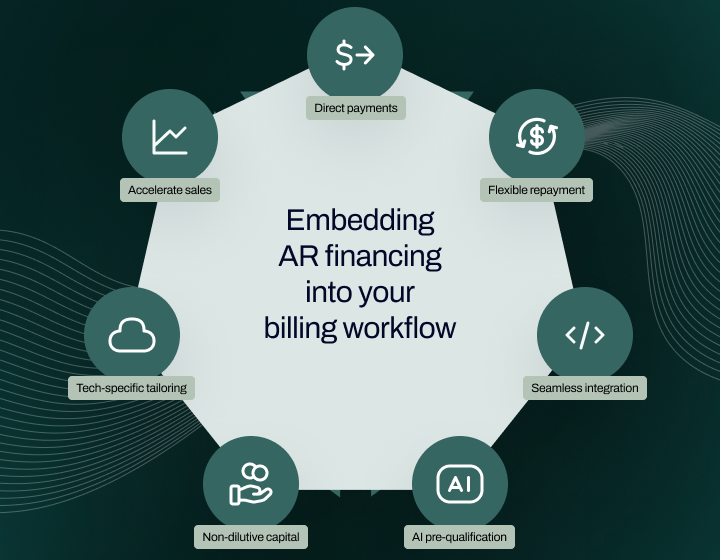

The Gynger Differentiation: Embedded AR / Payables Financing Tailored for Technology

Gynger offers a comprehensive accounts receivable and payables financing solution specifically designed for enterprise companies, delivering not only efficiency, flexibility, and operational integration, but also enhanced cash flow predictability, preservation of customer relationships, and fully transparent, adaptable repayment options.

1. Full-Invoice Payment, Direct to Vendors

Gynger ensures that vendors receive the full invoice value upfront, providing transparency and simplifying payment flows.

2. Flexible Repayment Methods

Flexible term options align payments with business cash flow cycles. Reimbursement capital and virtual card options further optimize working capital.

3. Embedded, Seamless Integration

No-code or low-code integration with existing accounting, CRM, and banking systems reduces administrative overhead.

4. AI-Powered Pre-Qualification

Instantly access flexible payment options for your business and your customers with AI-powered pre-qualification.

5. Non-Dilutive Capital

Gynger offers financing without equity dilution or burdensome covenants, preserving ownership and operational flexibility.

6. Technology-Specific Tailoring

Gynger is optimized for technology spending, including software, cloud, and hardware, ensuring appropriate underwriting and favorable terms.

7. Accelerating Sales for Vendors

Gynger enables sellers to offer financing to customers while receiving full payment upfront, enhancing sales efficiency and cash flow.

Receivable Financing vs Factoring: The Better Way With Gynger

Gynger’s solution allows companies to retain control over customer relationships while providing speed and flexibility, minimizing customer disruption, optimizing cost, and creating a sustainable long-term financing model.

Implementation & Considerations (From a CFO Lens)

- Credit Underwriting & Risk Assessment

Leverage Gynger’s AI-powered models for data-driven insights while maintaining prudent internal oversight. - Integration into Existing Systems

Ensure seamless connectivity for automated reflection in accounting and workflow systems. - Accounting & Reporting

Clearly define financing on the balance sheet and track key metrics such as DSO, DPO, and cash conversion cycle. - Customer Communication Strategy

Maintain transparent communications to reinforce customer confidence and continuity. - Scalability & Flexibility

Ensure the financing framework can adapt to increasing invoice volumes or expanding customer segments.

Optimizing Financing Strategy with Gynger

For growth-stage companies, the choice between receivable financing and factoring requires balancing control, cost, customer relationship management, and liquidity speed.

Gynger’s embedded financing model delivers a hybrid solution that maximizes flexibility, preserves customer relationships, and aligns with strategic growth objectives. Chat with our team to learn more about how Gynger can help you close cash flow gaps, free up working capital, and accelerate towards your growth goals.

Unlock the full article

This section is reserved for users. Sign in to continue reading or connect with our team to learn more.

Want to learn about how Gynger can help your business accelerate without compromise?

Get in touch

.jpeg)