Maintaining strong cash flow is critical, especially for companies with long payment cycles or enterprise clients that pay on 30, 60, or even 90-day terms. Accounts receivable factoring has offered a way to unlock working capital by converting invoices into immediate cash. However, while it remains a solution for many businesses, it is increasingly being reimagined or replaced by modern CFOs and finance leaders who are seeking more scalable, cost-effective, and technology-integrated approaches that build on its strengths while addressing its traditional limitations.

What Is Accounts Receivable Factoring?

Accounts receivable factoring, sometimes referred to as invoice factoring, is a financial transaction in which a business sells its outstanding customer invoices to a third-party company (known as a factor) at a discount. The business then typically receives 70% to 90% of the invoice value as an immediate cash advance.

Once the invoice is paid by the customer, the factor remits the remaining balance to the business, minus a service fee. These service fees vary but can range from 1% to 5%, depending on the invoice terms, client creditworthiness, and the agreement structure. In high-volume or lower-risk cases, rates may dip as low as 0.5% to 2% (The CFO Club).

Factoring is typically not a loan. It doesn’t appear as debt on your balance sheet and doesn’t require collateral beyond the invoice itself. This makes it an appealing option for businesses that are asset-light or don’t want to take on traditional credit obligations.

How Factoring Works:

- A company issues an invoice to a customer.

- The invoice is sold to a factoring company.

- The factor provides an advance, usually 70% to 90% of the invoice's value.

- The factor assumes responsibility for collecting payment.

- Once the customer pays, the factor deducts a fee and releases the remaining funds.

The Limited Benefits of Accounts Receivable Factoring

For many businesses, factoring offers a limited injection of capital:

- Immediate Liquidity: After setup, companies often receive advances of about 70%-90% of their invoice amount within 48 hours.

- No Additional Debt: Because it involves the sale of assets, factoring does not increase liabilities.

- Outsourced Collections: Some factors underwrite the customer and purchase the invoice outright, taking over collections.

- Credit-Based on Customer, Not Business: Startups or companies with limited credit history may qualify if their customers are creditworthy.

These characteristics can make factoring attractive for businesses with predictable invoice flows but slow-paying clients.

What Influences the Cost of Factoring?

Factoring rates are influenced by several components that can significantly affect the true cost of financing. Understanding these components is essential for CFOs and finance leaders evaluating accounts receivable factoring as a solution:

- Discount Rate: This is the base fee charged by the factoring company, often between 1% and 5%, depending on invoice volume, risk, and industry.

- Advance Rate: The percentage of the invoice value provided upfront, typically 70% to 90%, with the balance paid after customer payment minus fees.

- Duration of Collection Period: The longer it takes for your customers to pay, the more factoring can cost. Fees may accrue daily or weekly.

- Additional Fees: These include administrative fees, wire transfer fees, same-day funding charges, credit checks, and even monthly minimum usage fees.

- Type of Factoring: Recourse factoring generally has lower rates, but shifts non-payment risk back to your company. Non-recourse factoring shifts the risk to the factor but often comes at a higher price.

- Customer Credit Quality: Factors evaluate the creditworthiness of your customers, not just your business. Better client credit usually leads to lower rates.

Each of these factors plays into the total cost and structure of a factoring agreement. Businesses should request a transparent breakdown before signing any long-term deal.

Drawbacks and Limitations

Despite the limited advantages, factoring also comes with several drawbacks:

- High Costs and Add-on Fees: Factoring fees typically range from 1% to 5%, but additional charges, such as service fees, monthly minimums, termination penalties, and same-day wire fees, can add 1% to 2% more in hidden costs (The CFO Club).

- Upfront Costs: Factoring fees are deducted immediately from the advance, so businesses never receive the full invoice value upfront. This can overstate cash flow and limit reinvestment flexibility, potentially creating liquidity friction.

- Customer Relationship Impact: In disclosed factoring agreements, customers may be notified that payments are being collected by a third party. This can cause confusion or concern, particularly in enterprise or long-term client relationships.

- Contractual Commitments: Many factors require long-term contracts (1 to 3 years) and monthly invoice minimums. Failing to meet these minimums can trigger penalties or renegotiation.

- Recourse Risk: With recourse factoring, if a customer fails to pay, the business must buy back the invoice. This adds repayment risk to the business.

- Limited Fit for Tech and SaaS: Factoring assumes linear, invoice-based billing cycles. In subscription-based SaaS models or milestone-driven enterprise contracts, invoice factoring may not align well with cash recognition or ARR management.

The Market Today: A Growing But Evolving Solution

In the US, the factoring market reached over $171 billion in 2024. The U.S. market alone is expected to continue at a 9% CAGR through 2030 (Grand View Research).

Yet, this growth is also attracting scrutiny, especially from tech-focused CFOs who are seeking automation, control, and scalability. The demand is shifting toward solutions that are faster, more transparent, and embedded in the tools finance teams already use.

What Are The Alternatives to Factoring?

Factoring isn’t the only way to finance accounts receivable. In recent years, fintech platforms have emerged to offer a more streamlined, tech-first approach. Instead of selling invoices to a third party, companies can access capital through non-dilutive, software-integrated platforms that assess payment risk in real-time.

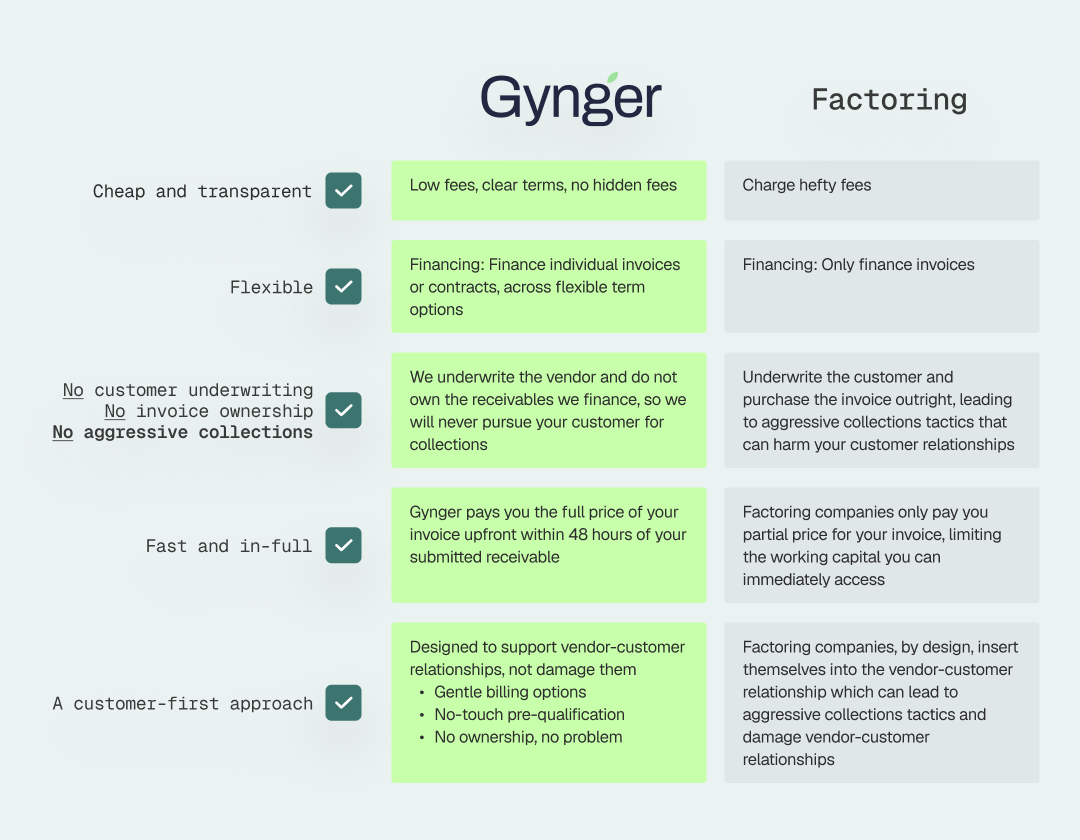

Gynger, for instance, is one such platform. Gynger provides upfront payment for tech purchases or receivables, offering finance on individual invoices or contracts across flexible term options. For vendors, this means getting paid faster without needing to sell invoices to factors, risk customer relationships, and pay large factoring fees. For buyers, it means flexible payment terms without tapping into credit lines.

Gynger is built for SaaS vendors, technology companies, and cloud infrastructure providers with their buyers and customers in mind, helping them successfully extend payment terms while sustaining access to capital today.

A Modern Approach to Factoring

Accounts receivable factoring may be a viable tool in the right context for businesses with limited financing options and a strong portfolio of receivables. However, its cost, complexity, and impact on customer relationships may make it less suitable for fast-scaling or tech-first companies.

For finance leaders, understanding the financial options is key to building a resilient, flexible capital stack that supports strategy and future growth.

Want to explore financing options that go beyond factoring? Visit Gynger to learn how modern AR and AP financing can work for you.

Unlock the full article

This section is reserved for users. Sign in to continue reading or connect with our team to learn more.

Want to learn about how Gynger can help your business accelerate without compromise?

Get in touch

.png)