.png)

Accounts receivable management is how businesses track, collect, and optimize payments owed by customers. It's a critical function that directly impacts working capital, cash flow predictability, and growth capacity. Yet even companies with strong AR processes face a persistent challenge that efficiency alone cannot solve.

Consider a familiar scenario. Your sales team closes a major deal. The contract is signed, the invoice sent, and revenue is recognized on your books. But when you check your bank account, the cash isn't there.

It won't be for 30, 60, sometimes 90 days or more. This timing gap between sales and cash collection has constrained businesses for decades.

Traditional accounts receivable management focused on improving collection speed through better invoicing, automated reminders, and disciplined follow-up. These approaches reduced manual work and improved efficiency. But they couldn't eliminate the fundamental wait. Even optimized collection processes still meant weeks or months before cash arrived.

Finance leaders faced an impossible trade-off: offer customers flexible payment terms and strain working capital, or demand faster payment and risk losing deals to competitors willing to be more accommodating.

Modern payment platforms are changing this dynamic entirely. By embedding financing directly into the payment flow, these platforms eliminate the traditional choice between customer flexibility and immediate cash access. Vendors receive full payment instantly while customers get the payment terms they need. The result transforms accounts receivable from a waiting game into instant cash conversion.

This guide explores how strategic accounts receivable management combines foundational best practices with modern payment technology to optimize working capital and accelerate growth.

Understanding Accounts Receivable Management

At its core, accounts receivable management encompasses the policies, processes, and technologies businesses use to ensure timely collection of customer payments. This includes everything from credit evaluation and invoice generation to payment processing and reconciliation. For CFOs and finance leaders, effective AR management directly determines how quickly revenue converts to usable cash.

The distinction between strategic and operational AR management matters significantly. Operational AR management focuses on execution: sending invoices, tracking payments, and following up on overdue accounts. Strategic AR management looks at the bigger picture. It examines how payment terms affect customer acquisition, how collection timing impacts growth initiatives, and how working capital efficiency creates competitive advantages.

Strong accounts receivable management drives business outcomes beyond the finance function. Companies that maintain shorter collection cycles preserve cash for investment rather than watching it sit locked in unpaid invoices. Better cash flow predictability enables confident decision-making about hiring, product development, and market expansion. Optimized AR processes reduce the administrative burden on finance teams, freeing resources for higher-value strategic work.

Traditional AR Management Process

The conventional AR management cycle follows a predictable path. Finance teams assess customer creditworthiness before extending payment terms. Once approved, invoices go out with specified due dates. Collections teams send reminders as due dates approach and follow up when payments run late. Finally, finance staff reconcile incoming payments against outstanding invoices.

This process can be efficient, but it cannot escape an inherent constraint. The timing gap between sale and cash receipt remains fixed by customer payment terms. A company with Net 60 payment terms waits two months for cash, regardless of how efficiently they manage the process in between.

Modern Payments-First Approach

Payment platforms that embed financing capabilities fundamentally restructure this equation. Rather than optimizing collection timing, these platforms eliminate the wait entirely. When customers select payment terms at checkout, the vendor receives full payment immediately while customers repay over their preferred timeframe.

This approach achieves what traditional AR management cannot: zero-day cash conversion. The concept of days sales outstanding (DSO) becomes effectively irrelevant when payments arrive instantly. Finance teams shift from managing collection cycles to managing payment options, a transformation that changes both strategic possibilities and operational focus.

Modern AR management is evolving from "how do we collect faster" to "how do we enable seamless payment experiences that serve both business and customer needs."

The Strategic Importance of AR Management

Accounts receivable represents more than an accounting line item. For growing businesses, AR management directly determines operational runway, strategic flexibility, and competitive positioning.

Direct Business Impact

Working capital efficiency begins with how quickly revenue converts to cash. Every dollar tied up in unpaid invoices is a dollar unavailable for growth initiatives. Strong cash flow management enables businesses to invest in product development, expand teams, and pursue market opportunities without constantly seeking external financing.

Consider the mathematics. A business generating $10 million in annual revenue with 45-day payment terms has roughly $1.2 million locked in receivables at any given time. Reducing collection time to 30 days frees up $400,000 in working capital. That capital can fund hiring, marketing campaigns, or infrastructure investments without diluting equity or taking on debt.

Customer relationships depend significantly on payment flexibility. Companies that offer rigid payment terms risk losing deals to competitors willing to accommodate customer cash flow needs. Yet extending generous payment terms without the right infrastructure strains your own working capital. This creates a strategic dilemma: prioritize customer experience or financial health?

Modern payment solutions resolve this tension by enabling both simultaneously. Businesses can offer the flexible terms customers want while receiving immediate payment themselves.

The Cost of Poor AR Management

The stakes are substantial. According to CB Insights research, 2 in 5 young businesses fail because they run out of cash. Revenue on the books means nothing if bills come due before customer payments arrive.

Cash trapped in receivables creates opportunity costs that extend beyond immediate liquidity needs. Businesses miss time-sensitive investments, delay critical hires, or pass on favorable vendor terms requiring upfront payment. The compounding effect of these missed opportunities can exceed the face value of the delayed receivables themselves.

Manual collection processes drain resources that could drive strategic value. Finance teams spend hours tracking invoices, sending reminders, and reconciling payments. This administrative burden scales poorly as transaction volume grows, eventually requiring additional headcount just to maintain existing operations.

Industry data reveals the performance gap. The average business collects payments in 36.6 days. Top-performing companies collect in 29 days, while typical companies take 48.8 days. This 20-day difference in days sales outstanding translates directly to working capital availability.

Industry-Specific Considerations for Tech Companies

Technology companies face amplified versions of these challenges. SaaS businesses manage complex subscription billing cycles and annual contracts paid monthly. Enterprise software companies navigate long sales cycles followed by extended payment terms. Cloud infrastructure providers balance usage-based billing with predictable cash flow needs.

These sector-specific dynamics make AR management even more critical for technology businesses, though the fundamental principles apply across industries.

Key Metrics for Accounts Receivable Performance

Measuring accounts receivable performance requires tracking metrics that reveal both efficiency and strategic impact. Traditional AR management optimized these metrics incrementally. Modern payment platforms can transform them fundamentally.

Days Sales Outstanding (DSO)

Days sales outstanding measures the average time between sale and cash collection. The calculation divides accounts receivable by average daily credit sales. Industry benchmarks vary significantly, with technology companies typically targeting 35-50 days while top performers across sectors achieve under 30 days.

DSO directly impacts working capital availability. Every day of reduction frees up cash equal to your average daily sales. A company with $100,000 in daily credit sales that reduces DSO from 45 to 35 days unlocks $1 million in working capital.

Payment platforms with embedded financing can effectively reduce DSO to zero by providing instant payment to vendors while customers pay over time. This represents a paradigm shift rather than an incremental improvement in a traditionally stubborn metric.

Collection Effectiveness Index (CEI)

CEI measures what percentage of receivables you successfully collect during a given period. The formula compares cash collected to the receivables available for collection. Strong performance typically exceeds 90%, indicating efficient collection processes and healthy customer payment behavior.

Lower CEI scores signal potential issues with customer creditworthiness, payment term management, or collection procedures. Modern payment platforms improve CEI by handling credit assessment upfront and managing repayment workflows automatically.

Cash Conversion Cycle

The cash conversion cycle measures how long capital remains tied up in operations before converting back to cash. For most businesses, DSO represents the largest component of this cycle. Optimizing cash flow requires managing the entire cycle, but accounts receivable typically offers the greatest opportunity for improvement.

Instant payment solutions collapse the receivables portion of the cycle entirely, fundamentally changing working capital dynamics.

Additional Performance Indicators

Accounts receivable turnover ratio tracks how many times per year you collect your average receivables balance. Higher turnover indicates efficient collection.

Average days delinquent measures overdue payment timing, providing early warning of credit or collection issues. Bad debt ratio quantifies uncollectible receivables as a percentage of total credit sales.

Modern payment platforms reduce the relevance of collection-focused metrics by eliminating the collection process itself.

Solving Common Accounts Receivable Challenges

Finance leaders consistently encounter the same fundamental AR challenges. Understanding how different solutions address these challenges reveals why payment transformation matters more than process optimization alone.

The Payment Timing Gap

The constraint is simple but consequential. Revenue appears on your income statement the moment you close a deal, but cash arrives weeks or months later. This mismatch between accounting recognition and actual liquidity creates planning complexity and constrains growth initiatives.

Traditional approaches focused on accelerating collections through early payment discounts, streamlined invoicing, and aggressive follow-up. These tactics might reduce payment timing from 60 days to 45 days, an improvement that still leaves substantial capital locked away.

Payment platforms with embedded financing eliminate the gap entirely by providing immediate vendor payment regardless of customer payment terms. The fundamental constraint disappears rather than improving incrementally.

Customer Payment Flexibility vs. Fast Cash

Companies traditionally chose between two unappealing options. Demand quick payment and risk losing deals to competitors offering better terms. Or extend generous payment terms and strain your working capital to accommodate customer preferences.

This trade-off affected more than individual transactions. It shaped competitive positioning, customer satisfaction, and growth capacity. Finance teams that prioritized collections often heard from sales about lost deals. Finance teams that accommodated customers struggled with cash flow forecasting and working capital management.

Different financing approaches handle this challenge differently. Traditional factoring sells your receivables to third parties, often notifying customers and potentially affecting relationships. Modern embedded financing provides instant payment while maintaining your customer relationships and brand experience throughout the payment process.

Manual Process Limitations

Labor-intensive AR operations consume finance team resources and scale poorly as transaction volume grows. Manual invoicing, payment tracking, reminder sending, and reconciliation create bottlenecks that require additional headcount as the business expands.

AR automation tools reduce manual workload significantly through automated workflows and system integration. Payment platforms take automation further by eliminating entire process categories. When vendors receive immediate payment and customers handle repayment directly with the financing provider, traditional collection activities become unnecessary.

Forecasting Uncertainty

Unpredictable payment timing complicates cash flow forecasting and strategic planning. Even with historical data, customer payment behavior varies based on internal factors that finance teams cannot see or control.

Better prediction models help, but instant payment eliminates forecasting uncertainty entirely. When cash arrives immediately upon sale, forecasting becomes a straightforward revenue projection rather than a complex payment behavior analysis.

.png)

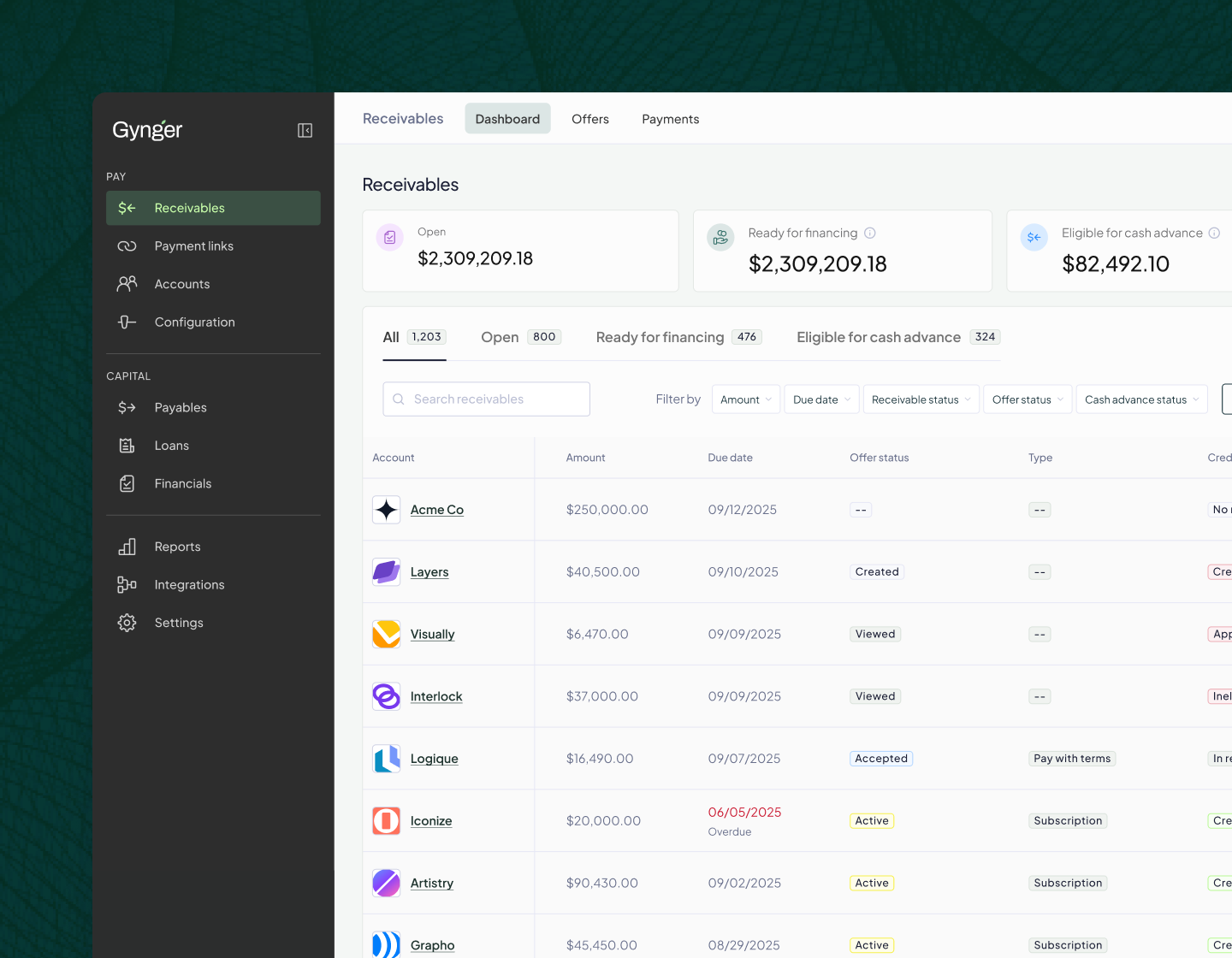

6 Best Practices for Modern AR Management

Strategic accounts receivable management combines foundational process discipline with modern payment capabilities. This section provides a high-level framework for AR optimization. For comprehensive implementation guidance, detailed credit policy frameworks, and CFO-specific strategic considerations, see our complete best practices guide.

- Establish Clear Credit Policies

Credit decisions drive both revenue opportunity and financial risk. Strong credit policies define risk tolerance parameters, approval thresholds, and documentation requirements without creating bottlenecks that slow sales. Modern payment platforms enable instant credit assessment through AI-powered evaluation, eliminating the traditional tension between thorough review and deal velocity.

Quick decision frameworks based on customer segments and transaction characteristics help finance teams respond rapidly while maintaining appropriate oversight.

- Optimize Invoicing & Documentation

Invoice accuracy and timing directly affect payment speed and customer satisfaction. Electronic delivery ensures invoices arrive immediately rather than sitting in mail systems. Clear payment instructions, detailed line items, and prominent due dates reduce customer confusion and payment friction.

Integration with payment platforms enables customers to complete transactions directly from invoices rather than navigating separate payment processes. This seamless experience improves payment timing and reduces administrative back-and-forth.

- Leverage Modern Payment Solutions

Payment flexibility has become a competitive differentiator in many markets. Traditional approaches like factoring enabled faster cash access but often required customer notification and created relationship complexity. Modern embedded financing provides instant vendor payment while maintaining direct customer relationships and brand consistency throughout the payment experience.

Sales teams gain flexibility to close deals with payment terms that work for customers, knowing finance receives immediate payment regardless. This alignment between sales objectives and financial requirements eliminates internal friction while improving customer experience.

- Implement Strategic Automation

Automation technology reduces manual workload across invoicing, payment processing, and reconciliation. The highest-impact automation focuses on repetitive, high-volume activities that consume significant resources but add limited strategic value.

Integration with existing ERP, CRM, and banking systems ensures data flows seamlessly without manual transfers or duplicate entry. Real-time synchronization provides accurate visibility into cash position and receivables status.

- Monitor Key Performance Metrics

Real-time dashboards tracking DSO, collection effectiveness, and aging reports provide early warning of emerging issues. Trend analysis reveals patterns in customer payment behavior and seasonal variations that inform strategic planning.

Modern payment platforms often provide enhanced visibility by eliminating the noise of traditional collection activities, allowing finance teams to focus on strategic metrics rather than operational tracking.

- Foster Cross-Functional Alignment

Effective AR management requires coordination between sales, finance, and customer success teams. Shared accountability for customer experience and cash flow creates alignment rather than competing priorities. Clear communication about payment terms, customer expectations, and financial requirements ensures consistent messaging throughout the customer lifecycle.

Technology's Role in Modern AR Management

Technology infrastructure determines what's possible in accounts receivable management. The distinction between traditional automation tools and modern payments platforms shapes both operational capabilities and strategic outcomes.

Payments Platforms with Embedded Financing

Traditional payment processors handle transaction execution. Payment platforms with embedded financing transform the entire payment relationship. These platforms assess credit in real time, provide instant vendor payment, and manage customer repayment independently.

The vendor experience changes fundamentally. Finance teams no longer manage collections workflows, send payment reminders, or reconcile customer payments. Instead, they receive full payment immediately upon sale and gain visibility into payment performance through unified dashboards.

The customer experience remains seamless. Payment options integrate directly into checkout flows with white-labeled interfaces that maintain brand consistency. Flexible terms accommodate different cash flow needs without creating vendor-side complications.

Platforms like Gynger demonstrate how embedded financing capabilities differentiate modern payment infrastructure from traditional AR automation, which optimizes existing processes rather than eliminating constraints.

AI & Machine Learning Integration

Artificial intelligence transforms accounts receivable from reactive operations to predictive strategy. Machine learning algorithms assess credit risk instantly by analyzing payment history, financial health indicators, and behavioral patterns across thousands of data points.

Real-time decision-making replaces multi-day approval cycles. Credit assessments that once required manual review now happen automatically within predefined risk parameters. Payment prediction models forecast cash flow with accuracy that manual analysis cannot match.

AI-powered optimization extends beyond credit decisions. Intelligent systems identify optimal payment terms for different customer segments, predict which customers need proactive outreach, and automate exception handling based on historical patterns.

Integration Ecosystem

Modern AR technology connects seamlessly with existing business systems. ERP integration ensures accounting data flows bidirectionally without manual intervention. CRM connectivity provides sales teams with real-time visibility into customer payment capacity and history.

Banking system integration enables automatic reconciliation as payments arrive. Real-time data synchronization across platforms creates a single source of truth for cash position, outstanding receivables, and payment performance.

These integrations eliminate data silos and manual processes that traditionally consumed finance team resources while reducing accuracy and creating delays.

The Future of Accounts Receivable Management

The trajectory is clear. Accounts receivable management is evolving from collection optimization to payment transformation, fundamentally changing what finance leaders can expect from their AR operations.

The Paradigm Shift

Zero-day DSO is becoming the performance standard rather than an aspirational target. As embedded financing capabilities mature and adoption accelerates, instant payment models will transition from a competitive differentiator to a baseline expectation. Businesses still operating traditional 30-60 day collection cycles will face increasing pressure from competitors who offer customer flexibility without sacrificing their own cash flow.

The question shifts from "how do we collect faster" to "why are we still collecting at all."

AI-Powered Autonomous Operations

Artificial intelligence continues advancing beyond current capabilities. Future AR systems will route payments intelligently based on real-time analysis of customer preferences, transaction characteristics, and optimal financing structures. Predictive models will proactively offer financing options that maximize conversion while maintaining appropriate risk parameters.

Autonomous reconciliation and exception handling will require minimal human oversight. Finance teams will focus on strategic decisions rather than operational execution.

Payment Optimization as Competitive Advantage

Early adopters of instant payment infrastructure gain measurable advantages. Financial flexibility enables a faster response to market opportunities. Sales teams close deals without artificial constraints created by payment term limitations. Customer experience improves through seamless payment options that accommodate varying needs.

As this technology becomes mainstream, businesses maintaining traditional AR approaches will find themselves at a structural disadvantage. The transformation from collection management to payment enablement represents a permanent shift in how modern finance operations function.

Transform Your Accounts Receivable Strategy

Accounts receivable management has evolved through three distinct phases.

- Traditional collection-focused approaches optimized invoice timing and follow-up workflows.

- Automation technology reduced manual workload and improved operational efficiency.

- AI agentic intelligence transformed decisioning, enabling real-time credit assessment, predictive payment behavior modeling, and autonomous exception handling

- Now, payment transformation through embedded financing eliminates the fundamental constraint between sales and cash availability.

Modern payment platforms enable both customer flexibility and immediate vendor payment, resolving a trade-off that constrained businesses for decades. Technology enables strategic outcomes that process optimization alone could never achieve.

The Gynger Advantage

Gynger delivers a payments infrastructure built specifically for modern accounts receivable requirements. Embedded financing capabilities provide instant payment to vendors while customers access flexible payment terms. AI-powered credit assessment enables immediate approvals without manual review bottlenecks.

- Zero-day DSO becomes an operational reality rather than an aspirational target.

- Sales teams close deals with payment flexibility that competitors cannot match without sacrificing their own cash flow.

- Finance teams eliminate collection workflows, payment tracking, and reconciliation complexity.

- The platform integrates seamlessly with existing systems through connections to ERP, CRM, and banking infrastructure.

- Real-time visibility into payment operations provides strategic intelligence without operational burden.

Ready to Transform Your AR Operations?

Gynger's payment platform converts accounts receivable from a collection challenge into instant cash conversion. Explore how Gynger enables immediate vendor payment with flexible customer terms, or contact our team to discuss your specific accounts receivable requirements.

Modern AR management is no longer about collecting faster. It's about eliminating the wait entirely.

Accounts Receivable Management FAQ

What is accounts receivable management, and why does it matter?

Accounts receivable management encompasses the policies, processes, and technologies businesses use to track and collect customer payments. It directly impacts working capital availability, cash flow predictability, and growth capacity. Effective AR management determines how quickly revenue converts to usable cash for operations and investment.

How do modern payment platforms differ from traditional AR automation?

Traditional AR automation streamlines existing collection processes through automated invoicing, payment reminders, and reconciliation. Payment platforms with embedded financing eliminate collection processes entirely by providing instant vendor payment while customers pay over time. The difference is transformation versus optimization.

What does zero DSO mean, and how is it achieved?

Zero DSO means vendors receive payment immediately upon sale rather than waiting 30-90 days for customer payment. This is achieved through embedded financing, where payment platforms provide upfront cash to vendors while managing customer repayment independently. Traditional DSO metrics become irrelevant when collection timing disappears.

How does embedded financing work in payment platforms?

Embedded financing integrates credit assessment and payment options directly into the purchase flow. Customers select payment terms at checkout, vendors receive full payment immediately, and the platform handles customer repayment. The financing infrastructure operates behind the scenes without disrupting the customer experience.

What's the difference between AR financing and factoring?

Factoring sells receivables to third parties, often notifying customers and potentially affecting relationships. Modern receivable financing provides immediate payment while maintaining direct customer relationships and brand consistency throughout the payment process.

How can I improve AR performance without hurting customer relationships?

Embedded financing in payment platforms enables both immediate vendor cash and customer payment flexibility. This eliminates the traditional trade-off between fast collections and customer accommodation. Sales teams can offer generous terms, knowing finance receives immediate payment.

What are the key metrics for measuring AR success?

Days sales outstanding (DSO), collection effectiveness index (CEI), cash conversion cycle, and AR turnover ratio provide visibility into receivables performance. Modern payment platforms can effectively reduce DSO to zero, fundamentally changing how these metrics function.

How do payment platforms integrate with existing systems?

Modern platforms connect to ERP systems, CRM platforms, and banking infrastructure through API integrations. Data synchronization happens automatically, eliminating manual entry and ensuring real-time visibility across systems without disrupting existing workflows.

Unlock the full article

This section is reserved for users. Sign in to continue reading or connect with our team to learn more.

Want to learn about how Gynger can help your business accelerate without compromise?

Get in touch

.png)